Borosil Renewables - Too Close To The Sun? ☀️

- Jun 10, 2023

- 6 min read

Whether it is the last son of Krypton or the most remote village of India - both parties benefit greatly from the power that our yellow sun possesses! In a country that gets 300 days of pure sunshine in a year, it’s only fair to use it to our advantage.

And India has been basking in that potential. As of 2023, solar energy is now the fastest-growing renewable energy source. With 67 GW of installed capacity, solar energy comprises of just 5% of the total energy production in India. However, it has grown at a 60% CAGR over the last 5 years, compared to the 4% CAGR in overall electricity production.

There’s no stopping here. India intends to cross 200 GW in solar capacity over the next 5-7 years, which is 3x the current capacity. And tripling of capacity means a proportionate expansion for solar panels - the key device that converts sunlight into electricity.

Speaking of solar panels, they consist of a fair amount of parts like an aluminium frame, tempered glass, solar cells, and junction box at the base. Although solar cells are the most important part of the panel, the 2-4mm thick solar glass is what protects the cell and traps the heat to facilitate power generation.

And, India houses the company that has made huge strides in the innovation and manufacturing of this piece of glass - Borosil Renewables! From making dinner sets and bowls, this leg of the company has grown into the first and largest solar glass manufacturing company in India. The stock has skyrocketed by 12x in 5 years!

With solar power generation set to grow 3x, what’s next for Borosil Renewables? 3x returns? Maybe not.

The Chinese Are Winning

Unfortunately, in every good story there is an antagonist, and for Borosil Renewables it was our neighbours from the North-East - China. With a 97% market share in solar glass globally, just two Chinese companies dominate the entire world market.

Naturally, the scale, expertise and efficiency that the Chinese bring to the world market had to affect India as well. In India, Chinese players have a 60% market share in the solar glass market, thanks to two factors:

Predatory pricing By selling their products at ridiculously cheap rates (discounts of up to 15% to Borosil Renewables’ prices), the Chinese players were able to “dump” its product, a practice that is looked down up in international trade standards since it adversely affects the domestic players of a country, a.k.a, Borosil.

Basically, if Borosil Renewables was pricing the solar glass at around Rs. 450 per square meter, China priced it at Rs. 380 - and who doesn’t want to pay lesser for a product of similar quality!

Demand-supply gap While solar energy production in India grew multi-fold, India’s solar glass manufacturing capacity could serve only a fraction of the demand. In fact, Borosil Renewables set up the first solar glass plant in India in 2010 (180 TPD capacity or about 1.26 GW).

China was quick to fill the void, and bombarded the solar glass market of India, gaining an 80% market share by 2017.

Government to the Rescue

With China flooding the Indian solar glass market, Borosil Renewables did something that could be considered nerdy but was necessary - it complained to the Directorate General of Trade Remedies to impose anti-dumping duties on the various Chinese companies involved in these unfair practices (dumping).

The DGTR then took it up with the Ministry of Finance, which then imposed duties to the tune of Rs. 4,000 - Rs.10,000 per metric ton of solar glass imported. Coupled with longer delivery times and freight charges of Rs. 2,00,000-Rs. 3,00,000 per container, Chinese players started to wane off the Indian markets for the 5-year duration of the duties.

What followed in the next 4-5 years was nothing short of historic for Borosil Renewables, tracking the pricing of Chinese players and offering a slight discount to remain competitive (China at Rs. 488 per square meter and Borosil Renewables at Rs. 466 per square meter).

Since it was the only large solar glass manufacturer at the time, it had smooth-sailing, adding capacity to about 450 TPD (2.5x from when it started), and was supplying to 95% of the 250 solar developers/module manufacturers in India, with customers like Adani, Tata Power, Renew, Emvee, Waree, and Vikram Solar making the list.

The result was a massive push to its income statement, balance sheet and stock price, all of which recorded such marvellous numbers that will instantly make you feel the FOMO for having not invested in this company:

But the Indian Market Needs China

Unfortunately for Borosil Renewables, the story wasn’t over here, and the happy ending was no where near. Borosil Renewables was still at the top of its game, adding further capacity in FY23, bringing its domestic capacity to 1,000 TPD, still enjoying the pleasure of being the largest manufacturer of solar glass in the country.

But fun times started to fade sometime last year (end of 2022), as the 5-year duty period ended, leaving Chinese players free to be back to their antics of selling at exceptionally low costs without having to pay those dumping duties anymore.

Borosil Renewables tried to file another petition to levy higher anti-dumping duties and urged the Ministry of Finance to even revise an age-old exemption given to China from 1999 against certain customs and import duties, but there has been blatant rejection of those petitions.

A major reason could be the sheer reliance on the Chinese supply for the needs that India has for solar panel manufacturing to meet the power demands of the country. With the current demand of around 3,000 tonnes of glass per day, Borosil Renewables, being the largest player in the country, services about 35% of that with its current capacity. With no other major players to fulfil that demand, there comes an obvious ned to turn to the cheaper imports from China.

The Chinese comeback, rising cost of fuel prices and raw materials and the need to remain competitive while adding capacity resulted in profitability taking a hit in FY23:

Any Chance for Borosil Renewables to Win Then?

As a company, yes. As a stock, maybe not.

Over the next 4 years, the Indian solar market is set to grow 3x. There of course is room for growth. But provided Indian players are able to install capacity for solar glass as fast as solar power generation capacity is increasing.

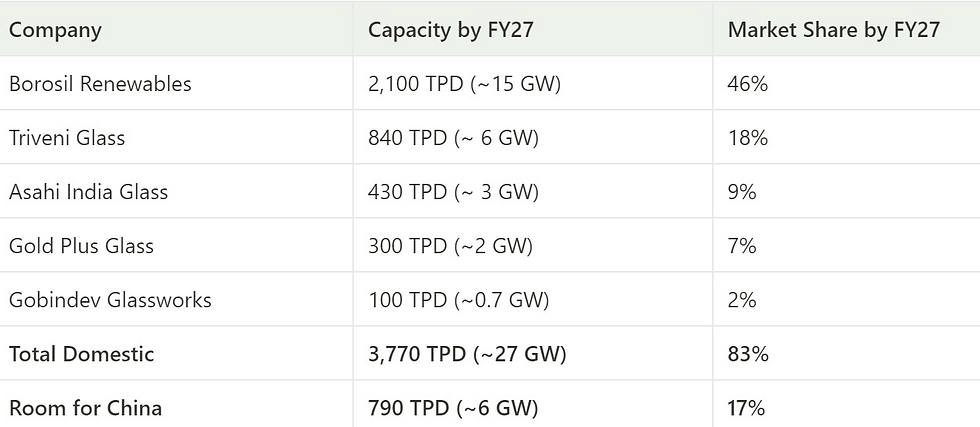

With such a large opportunity in place, multiple Indian companies, including Borosil Renewables have announced plans to add/increase capacity by FY27. However, even with aggressive capacities coming in domestically, Indian players will still not be able to fully meet demand.

Of course, the situation will get better with India being able to fulfil 83% of demand by FY27 versus only 35% now.

Over this four year period, Borosil Renewables is expected to continue exhibiting strong numbers:

Capacity is expected to more than double to 2,100 TPD by FY27, from 1,000 TPD now

The capacity addition is likely to result in a 21% revenue CAGR, as pricing remains tight, making revenue growth hinged on to volume growth

While EBITDA margins are currently pressured by high power costs and raw material expenses, inflation cooling off is expected to aid margin expansion from 18% in FY23 to 22% in FY27

Consequently, PAT is expected to grow at a 24% CAGR

What’s the Problem with the Stock Then?

At Rs. 540, the stock is trading at a one-year forward PE of 76x. This could be perceived as expensive given:

The government has not extended anti dumping duties on to Chinese players, leaving Borosil Renewables in a place where it has to drawback on the higher prices it enjoyed between FY18 and FY23

The fact that the government had introduced duties in the first place made the space appear lucrative, and attracted several domestic players to add capacity. This would lead to Borosil Renewables’ monopoly amongst the Indian players, going to down to a 46% market share in the next four years

While growth still remains high at a revenue and PAT CAGR of 21% and 29% respectively over the next 4 years; it is lower than the revenue and PAT CAGR of 42% and 29% seen over the last 5 years

With Borosil Renewables having spent money on acquiring capacity in Europe, its expansion plans in India got delayed, and it now expected to operationalise capacity only in FY26/27, which makes it incapable of fully utilising the Indian market opportunity until then

Before Borosil Renewables and other Indian players add capacity and take share back, China’s share could peak out at 75% (from the current 65%) as soon as next year, resulting in interim negative news flow

Large players like the Tata Group and Adani Group have been making news for their plans of end-to-end module manufacturing (including cells and glass), which could just be a stronger and more economical proposition, putting piecemeal manufacturers at risk of losing share

Because of all these factors, there is a threat to the expensive valuations of Borosil Renewables, which is currently trading at 4x PEG. However, if the stock were to fall further over the coming months because of any of the above factors, its valuations could seem reasonable given the long term opportunity, strong industry tailwinds, demand-supply gap and consequently strong financial performance.

While Borosil Renewables still remains a dominant force in the solar glass industry, unmatched in market leadership, reach and capacity, it looks like it has flown too close to the sun lately, but whether it meets the same end that Icarus did is a wait-and-watch game as always!

Comments